By Khadijah Abu and Yvonne-Faith Elaigwu

Introduction

Traditionally, most financial products and services were designed without consulting customers or truly understanding their peculiar needs. Product designs and features were rather focused on what technology can do – highlighting new features and innovation which may not address the core of customer needs. Hence, the idea of placing the customer at the centre of product and service design remained conceptual – the outcome being products and services that neither optimise customer engagement nor utility.

However, in an open banking model, players within the ecosystem will drive value by supporting customers through the delivery of contextually and uniquely relevant experiences. To effectively do this, financial institutions and third parties in the ecosystem actively obtain, interpret, and utilise feedback from customers.

Customer-centricity is an open banking model is underpinned by customer experience that is data-led and transparent, empowering customers to a better control of their finances and personal data. It signifies an unprecedented level of focus on customers, providing them with the choice to share their personal and financial data with the companies that provide the most favourable service options – hence putting the customer in the driver seat.

Customer-centric systems transcend customer experience informed by ideals – they are built to push forward solutions that are contextually relevant based on a deep-rooted understanding of customer’s actual needs, behaviours, and aspirations.

In this article, we provide insights on customer requirements and customer-centricity in the open banking model including the contextual relevance to Nigeria.

“You have to start with the customer experience and work backwards to the technology”

– Steve Jobs

Customer requirements as a driver for customer-centricity in an open model

With the emergence of alternative payments, customer considerations in choosing payment methods were categorised into 3 key requirements;

Reach – whether the payment method enables customers to reach their counterparty i.e. whether payers and payees can actually interact.

Conversion – How fit a payment method is for the customer’s intended purpose.

Cost – How much it costs in terms of fees for using a particular payment method.

The chosen payment methods were mostly the ones that balanced reach, conversion and cost the best. However, in the wake of technological developments in the industry and the need to respond to customer needs, it has become obvious that banks based on their infrastructure have created a trusted ‘reach’, however showing gaps in ‘conversion’. Third-party players such as Fintechs on the other hand, have mostly addressed the ‘conversion’ needs of customers by providing products and services with advanced functionalities, however, lacking in ‘reach’. The open banking model provides a solution to this problem – forming a connection between banks, third party providers and customers.

In the open banking model, two out of the three overarching pillars of customer requirements – ‘reach’ and ‘conversion’ – are redefined.

From the perspective of customers in an open model, ‘reach’ refers to the numerous options they have as to which third party services they can connect to their bank accounts. Hence, ‘reach’ implies interoperability between parties in the ecosystem based on agreed standards in technology and practices.

‘Conversion’ refers to customer experience – the ease with which customers can use third-party services, particularly the ease of securely connecting and managing financial and personal data between bank and third-party interfaces.

The open banking model combines ‘reach’ and ‘conversion’ in such a way that customers are able to choose both propositions offered by banks and functionalities provided by third parties in the context of controlling their finances and personal data. Thus, from the customer’s perspective, adopting an open banking model translates to “choice and control”.

“A customer-centric model is based not on expertise in the realm of product development, but rather on a deep understanding of what customers actually want, when and how they want it, and what they’re willing to give you in exchange”

– Peter Fader

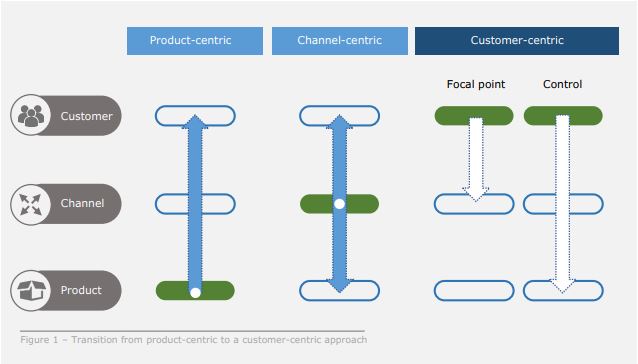

The shift to customer-centric systems in an open model

In the open banking ecosystem, the concept of customer-centricity is elevated from merely positioning the customer as the focal point for products and services to customers being in control, providing a continuous feedback loop through multiple channels. Hence, customers are in control over;

- The products and services they consume in relation to their banking needs

- The service providers they wish to buy the product or service from.

Figure 1 below, captures the shift from product-centric systems to customer-centric systems.

Active engagement with customers in their environment is an embedded feature of customer-centric systems – using behavioural tools to uncover deep insights that will inform solution designs. Technology only becomes the tool to unlock the insights drawn from customer engagement. Examples of ways customers may choose to explore the opportunities in the open model include;

- Connecting third-party apps to their bank accounts and vice versa e.g. to initiate payments

- Connecting bank account data to apps e.g. for personal financial management and credit

- Sharing or confirming personal attributes (e.g. email, name, age, etc.) to third party websites after authorisation with existing banking credentials

- Logging in to third party platforms after authorisation with existing banking credentials

What does this mean in the Nigerian context?

The demand for more contextually relevant products and services from banks and other financial institutions is not unique to the western world. Bank customers in Africa and Nigeria, in particular, are not left out. This is evidenced by the evolution of customer groups in Nigeria, triggered by several factors such as increasing rate of mobile phone penetration and smartphone adoption, growing middle-class population and the increasing relevance of digital in everyday life.

A study by GSMA shows that Nigeria has about 97 million unique mobile subscribers leading to a mobile phone penetration rate of 49%. In addition, there are about 53 million smartphone connections, resulting in a smartphone adoption rate of 36%. This is projected to 144 million smartphone connections by 2025. The level of mobile phone penetration has encouraged the uptake of digital services by businesses and consumers, impacting overall daily life in Nigeria. Also, Nigeria’s middle class has grown to about 23 percent of the population from roughly about 10 per cent in the last decade.

The impact of these factors has led to the emergence of unique customer groups in Nigeria based on their needs and expectations. Per group, their primary needs and buyer values for financial services are varied. However, the currently closed banking model continues to offer generic service/product propositions which limit the customer’s ability to choose or control their financial assets.

Take, for example, the Nigerian adult population within 18 to 35 years. This sub-category constitutes about 40% of Nigeria’s population. A closer look at their collective profile reveals common characteristics in their lifestyles. They;

- Are digitally focused and live a virtual life within the social space. Along their key life phases such as starting a job, starting a family, admission into schools, etc., they have embraced digitized experiences

- Are more vocal and less patient. They demand quick, consistent and convenient services. Their switch rate is also high and they are more in control of service options they choose

- Are becoming unresponsive to traditional sales approaches, but respond to more targeted and contextually relevant propositions. They expect to be met in their domain of activities

- Seek more options for customisation and self-service

- Wield influence over their peers

- Are more informed, less loyal and innovation-oriented. They only align to service or product options that propose the most value

As a result of the need for more personalization, asides cost considerations, customers within this category also prioritise reach and conversion. An underlying factor to their buyer values is the need to control what they consume and the need for multiple options in choosing services and/or products.

In the current banking model, most banks in Nigeria struggle with understanding unique customer needs and responding with local value propositions that are contextually relevant. For example, the bottom mass market in Nigeria – comprising over 60% of the market – has been largely under-served or unserved mostly because banks either do not understand the needs of this segment or are not organizationally configured to meet these needs.

So how will open banking redefine customer focus in the Nigerian banking system? The open model will propel banks and third-party providers in Nigeria to invest more in consumer-focused research to uncover key behavioural attributes of customer segments in Nigeria and understand how customers would rather consume financial services/products. It will position banks and third-party providers in the ecosystem to receive critical feedback at the speed of change in consumer preferences and expectations. Hence, the need to provide personalized services and products will embed the impact of socio-cultural factors on buyer values. For example, this feedback system will reveal why a typical merchant in the eastern part of Nigeria would consider a financial option over another, the motivations behind the customer’s choices, the information he has access to before making a buying decision and the questions the customer would raise while making decisions. Furthermore, the open banking model as a customer-centric proposition will support ecosystem participants to specifically serve chosen unique segments such as the bottom mass market.

Built on transparency, the open banking model will empower customers to demand more from players in the ecosystem, thus forcing them to re-think their customer journey mapping and customer experience strategies towards providing a healthy balance of cost, reach and conversion requirements of customers.

Conclusion

Open banking might mean different things in several quarters however there is universal agreement on its potential to fundamentally re-shape customer experience in banking and the wider financial services space.

“Open banking may have begun with a whisper, but that quiet beginning will soon give way to a roar of financial change”

– Matt Stroud

Businesses that will win in the era of Open Banking are those with an “unwavering” focus on driving customer value by providing products and services that truly embrace customer’s preferences, attitudes, and aspirations. The key to unlocking the enormous potential of an open model lies in understanding what customer’s needs are – involving customers from the onset – and not only on what technology can do.

The Open banking model redefines customer-centricity by creating new opportunities for customers – a better view of potential options – thus empowering consumers to find the best combination of products and services that suit their needs.

References

- Euro Banking Association- Open Banking: Advancing customer-centricity https://www.abe-eba.eu/media/azure/production/1355/eba_open_banking_advancing_customer-centricity_march_2017.pdf

- Nordea Open Banking – https://medium.com/@NordeaOpenBanking/open-banking-whats-in-it-for-customers-352d9b9f5011

- Software Insights – https://www.softwire.com/insights/why-open-banking-demands-a-truly-customer-centric-approach-to-designing-services/

- GSMA – Spotlight on Nigeria: Delivering a digital future