by Ope Adeoye, Brendan Playford and Oge Okonkwo

Introduction

Nigeria has a huge credit gap, with lenders and borrowers facing a number of challenges which hinder the ease of providing and accessing credit. This credit gap has contributed to curbing financial inclusion and economic growth. Open banking can transform lending in Nigeria by improving access to credit which would drive economic growth. This article showcases an illustrative use case of how open banking can be used to transform lending in Nigeria and address the issues currently faced by lenders and borrowers in order to drive credit. The use case demonstrates, step-by-step, a typical customer journey and how open APIs will be used to significantly improve the lending process.

Background

Credit is one of the most important parts of life and of every economy. Credit leads to an increase in spending and consumption which directly impacts income levels for every economy. Increased access to credit contributes to increased GDP which in turn accelerates long-term economic growth. Research has shown that countries with very limited access to credit have high poverty rates and are unable to continuously grow the economy. This is evident in a lot of developing countries, including Nigeria, which is characterized by a paucity of credit and poor quality of life for most of the country’s population.

While Nigeria has considerably grown its credit in recent years, largely driven by increased lending activity by commercial banks and the proliferation of FinTech lenders, the credit gap in the country is still estimated to be about NGN 51.8 trillion. This huge credit gap has impeded the growth in financial inclusion and consequently curbed economic growth. To remedy this, stakeholders within the financial ecosystem have different roles to play in addressing the credit gap and increasing access to credit in the country. Lenders, for example, must improve credit risk management and reporting in order to fully understand borrowers and provide innovative credit products that will be tailored to the needs of borrowers.

In developed countries, lenders conduct a detailed risk assessment, leveraging the credit score and financial history of the borrower to ascertain creditworthiness and the risk profile of the prospective borrower. This helps to identify the loan amount that fits the borrower’s risk profile, thus reducing the occurrence of loan defaults. In Nigeria, credit risk assessment and reporting are not holistic as it relies on only internal transactional data and reports from credit bureaus which most times are not adequate to provide a detailed view of a borrower’s financial health

Current issues faced by lenders

- Access to Credit Bureau data is expensive – Due to Nigeria’s prevalent low-income class (67% of the population), a lot of consumer loans are nano loans (below NGN 10,000). The cost of processing these loans, right from loan origination to credit risk assessment, is typically high. Access to credit bureau data is still expensive; costing as much as NGN 200 per nano loan where more than 90% of the loan applications might be rejected. With CBN capping loan management fees that can be passed on to borrowers at a maximum of 1% of loan amount disbursed, most of the loan processing fees are borne by the lenders, especially for nano loans. Also in the case where a loan application is rejected, the lender bears all the cost for loan origination and credit risk assessment.

- Access to statement data is expensive – In addition to the high cost of processing nano-loans, it is expensive for lenders to access bank statement data from other financial institutions. Obtaining a bank statement for a loan applicant can cost between NGN 250 – 400, depending on the format of the statement. This increases the cost that the lenders would have to bear, especially for nano loans.

- Unreliable technology (buggy and unreliable APIs) – When statement data or other financial data from third-party financial institutions are available, the API implementation is mostly buggy and unreliable, leading to the input of low-quality data into risk assessment models. There is currently no standard framework that drives API interaction within the Nigerian financial ecosystem. Data currently exist in silos, with each participant implementing their own APIs which are mostly not interoperable across the ecosystem.

- High default rates – Due to limited access to customer information across the financial ecosystem, lenders currently don’t have a full view of customers’ financial health. Hence, it is difficult to accurately identify and separate potential borrowers that will have difficulty in paying back their loans from those that won’t. Also, borrowers paying back their loans using cards can be unreliable most times. These card debit transactions linked to loan repayments fail at times and borrowers have to leverage other channels (bank direct debit mandate, mobile payment, in-branch bank payments etc.) to make loan repayments. This limits seamless loan repayment transactions and contributes to loan defaults.

- Limited ability to scale – In order to adequately address Nigeria’s credit gap, lenders within the financial ecosystem need to scale, increasing their growth and ability to provide loan products to an increasing customer base. This, however, seems to be difficult due to factors such as the high cost of processing loans, poor credit reporting and inadequate technology and legal infrastructure.

Current issues faced by borrowers

- Access to credit is difficult and inconvenient – Credit in Nigeria currently favours borrowers with rich credit and financial information history due to the ease which such data can be accessed by credit bureaus and financial institutions. Borrowers with ‘thin credit files’ (potential borrowers with limited or no credit history), however, often find it very difficult to access loans and are automatically excluded. Considering how Nigeria’s adult population is mostly unbanked (60.3%), it is imperative to understand that the larger portion of borrowers that require access to consumer credit might have thin credit files. Thus, lenders need to assess and score borrowers based on a wide range of information (phone usage and billing history, energy usage information, trends in income and expenses etc.) in order to financially include the underbanked.

- Difficulty in providing bank statements to lenders – It is cumbersome and expensive for borrowers to obtain statements of their financial transactions and share with lenders. Most times, borrowers have to pay to provide bank statements to lenders, paying as much as NGN 400 or more when all the borrower needs is a nano-loan of less than NGN 10,000.

- High cost of loans – Due to the high cost of processing loans (loan origination and credit risk assessment) and the pervasive occurrence of loan defaults, lenders have kept loan prices (interest) high enough to cover the risk of loan defaults. This, however, has led to loan products being less attractive and borrowers repaying loans with high-interest rates.

- Data Privacy – Carrying out a risk assessment for borrowers these days requires the use of certain API providers (such as credit bureau API check) which means customer data and information about their credentials are shared with third parties, which can be unsafe. There is currently no framework (such as open banking) in Nigeria to guide how data is shared to ensure it is safe and customer credentials are protected. This thus increases the risk of a data privacy breach.

How to solve these issues using open banking

Open banking is defined as the use of open technologies by financial institutions and third-party providers (TPPs) to share data in a standard format to provide more open, transparent, and competitive financial services. With open banking, customers must give consent to their banks and other financial institutions to share their data residing on internal systems of these banks and fintechs with third parties. This data can be used by lenders to gain a detailed view of a customer’s financial health, including information on assets, liabilities, deposits, investments, and transactions across all financial institutions and third parties. Lenders can consolidate this information with additional data from other third parties such as phone usage and billing history from Telcos, energy usage history from energy companies, shopping trends from retailers etc. in order to fully understand the customer and provide the right loan products tailored to each customer.

Open banking will solve the issues that are currently faced by Nigerian lenders and borrowers. Due to the open APIs, data will be readily available to relevant participants of the ecosystem who have the customer’s consent to access the data. These participants can then leverage digital technologies such as analytics to conduct a detailed risk assessment in real-time to ascertain the financial health and risk profile of each borrower and identify the loan amount which the customer will be able to easily payback.

With open banking, credit will be more available and competitive, which would have a huge impact on closing Nigeria’s credit gap for retail consumers and businesses, thus enhancing financial inclusion and economic growth.

Why open banking is a superior method for solving these problems

- Open banking is cheap and affordable to lenders and borrowers. Due to open APIs and access to rich customer data, the high cost of processing loans (origination and credit risk assessment) is immensely reduced. With the much-reduced cost of processing loans, lenders can provide loans with low-interest rates which would be very attractive and more affordable to borrowers.

- Open banking improves credit risk assessment and reporting. Credit risk assessment and reporting are key processes within the lending value chain. Availability of a wide range of data from multiple parties contributes to the quality of credit risk reports generated by lenders and credit bureaus. With open banking, lenders understand the financial health of potential borrowers – even more than the borrowers understand themselves – and can conduct a more informed credit risk assessment and reporting.

- Lending with open banking is very secure. Open banking is guided by a standard format of sharing data using open APIs and is largely driven by customer consent. This presents a more secure mode of data interaction as opposed to point-to-point buggy and atypical APIs between financial institutions. Adopting open banking will bolster cybersecurity as Nigerian financial institutions and third-party providers will work with standardized and secure API gateways as against custom and proprietary systems that could have hidden vulnerabilities.

- Open banking eliminates the need for ‘screen scraping’. Screen scraping refers to customers providing banking credentials (such as username and password) to third parties in order to share their data and access these third-party services. These third-party companies typically create a login page with a very similar look and feel as a bank’s online login page. The customer enters their login details which the third party can use to log in as the customer. Once logged into the account as the customer, screen scraping tools copy available data to an external database or system and can be used outside of the financial institution. A real-life example is a customer who requires financial budgeting and advisory services being provided by a Fintech but has to provide his/her banking credentials to enable the Fintech gain access to the customer’s financial data. This can be insecure as the customer’s financial information can be compromised in the case where the third party experiences a breach. With open banking, third parties will have no access to a customer’s login credentials or other sensitive data. Retrieving customers’ data in an open model is safer and more secure than screen scraping. Sharing and retrieving data using open APIs is also more reliable and faster, thus eliminating the need to depend on screen-scraping to share data.

- Open banking is standardized and not proprietary to any single company. One of the benefits of open banking is its ability to drive innovation and improve competition within the financial ecosystem. Open banking is a standard format that stands to benefit all stakeholders (regulators, banks, customers, fintechs, third parties etc.) and is not a technology or framework that is proprietary to any single company or group of companies. This means that there are endless opportunities that every participant of the lending value chain can take advantage of.

- Open banking will provide customers with better experience. Open banking will solve the current issue of inconvenience and poor user experience being faced by borrowers. Due to lenders gaining a better understanding of prospective borrowers, they will be able to provide differentiated loan products and services across channels. Also, open banking will create opportunities for loan aggregators to provide multiple loan products from different providers and create choices for borrowers where they can choose the most innovative and attractive offer.

Lending in the open banking era – Use Case

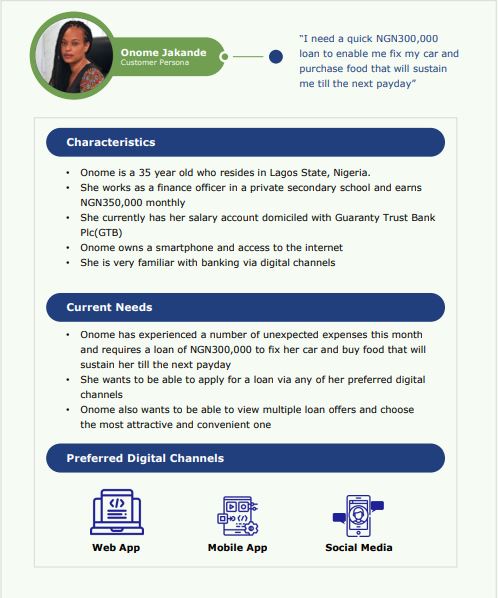

We have developed a fictitious use case of how lending can work in the open banking era. A customer persona has been defined to highlight the characteristics and needs of a typical customer.

From the fictitious customer persona above, Onome Jakande is a 35-year old accountant who resides in Lagos State and earns NGN 350,000 monthly. She has experienced several unexpected expenses this month and needs a loan of NGN 300,000 to fix her car and spend on food till the next payday. She currently banks with GTB and intends to apply for a loan with a lending company, using a loan aggregation app, ‘Open Credit’ (Open Credit is a fictitious app and only exists for the purpose of this use case).

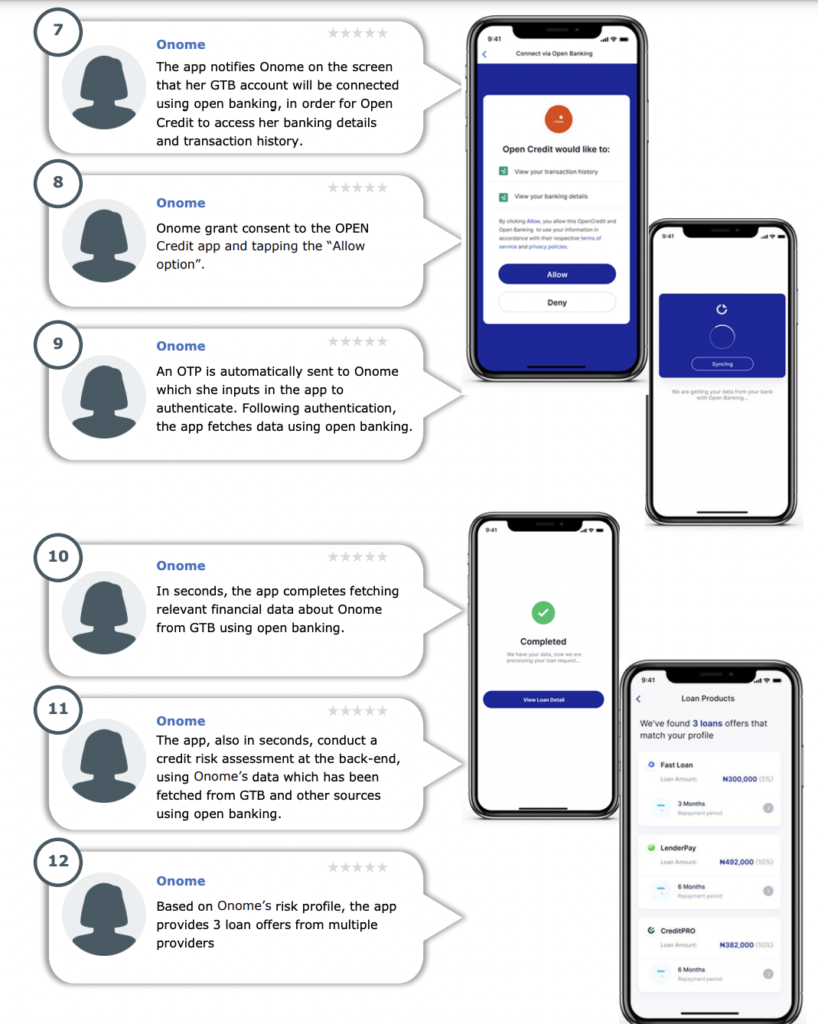

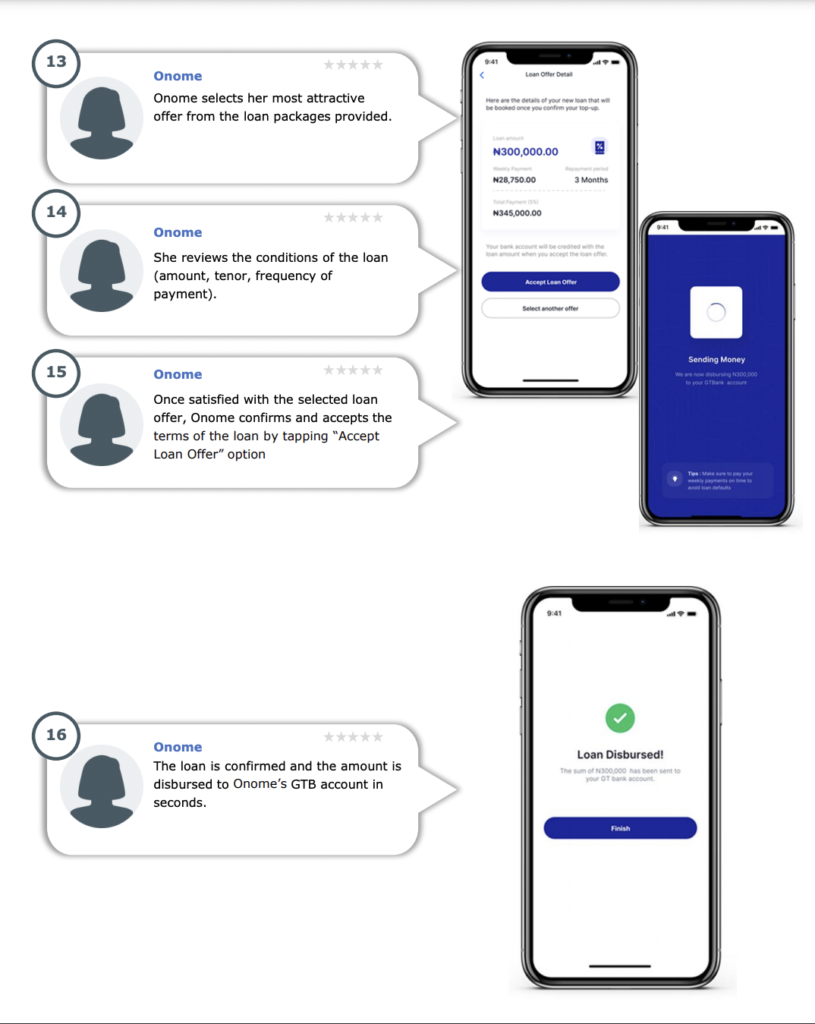

Due to the ease of sharing data in an open model, Onome will be able to consent to sharing her data with ‘Open Credit’, which can then leverage that data to conduct a real-time detailed credit risk assessment to ascertain her risk profile and provide loan offers that are tailored to her needs.

Conclusion

Open banking is set to transform the way Nigerians provide and access loans. Open banking addresses the myriad of issues currently faced by lenders and borrowers. With open banking, the cost of processing loans is much lower, credit risk assessment and reporting are much better, lending is very secure, and customers enjoy a much better user experience.

The adoption of open banking will contribute immensely in closing the Nigerian credit gap, enabling a lot more Nigerians access loans to meet short-, medium- and long-term needs. This will drive spending and consumption, increase income levels and enable long-term financial inclusion and economic growth.

References

- Banu, I.M., 2013. The impact of credit on economic growth in the global crisis context. Procedia Economics and Finance, 6, pp.25-30.

- Velpuri M, Sharma M, Maringanti C, Pidugu A and Velpuri J Improving Access to Credit in Property Markets Using Blockchain – FIG Proceedings (2017) [online].

- Central Bank of Nigeria (CBN) – Guide to Charges by Banks and other Financial Institutions in Nigeria [online].

- EFInA Access to Financial Services in Nigeria 2018 survey