by Adedeji Olowe and Oge Okonkwo

Introduction

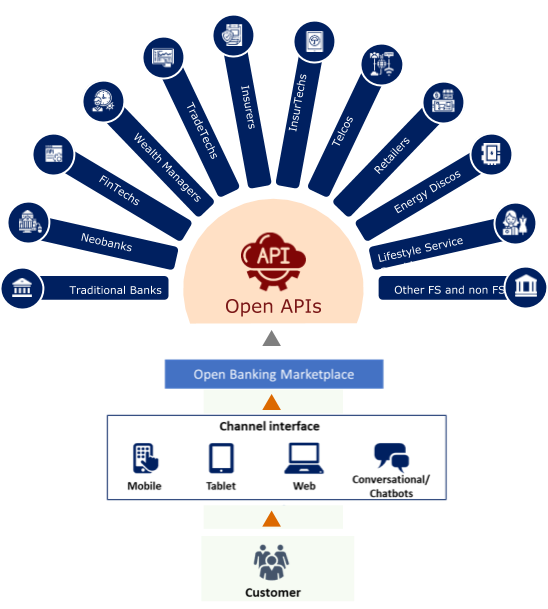

The concept of Open Banking is emerging globally as the potential future of the banking industry. Open banking refers to how financial institutions and third-party providers (FinTechs, InsurTechs, Lifestyle service providers, Retail companies, Telcos, Energy companies etc.) leverage open Application Programming Interfaces (APIs) to share data in a standard format to drive open, transparent, innovative and competitive banking services. Innovative traditional banks, FinTechs, agile neobanks, and digital disruptors are shaking up traditional banking rules, taking advantage of Open Banking, to spark cross-industry collaboration and the creation of exciting new channels for customers.

Open banking is good news for customers, on the grounds that an open banking model will enable them to gain easier access to a wider array of financial services offered by a larger selection of providers. With open APIs, customers can choose to share their financial information with other financial institutions and third-party providers, in order to access personalized product and service offerings. Open APIs will make it much easier for banking customers to transfer their accounts, manage payments, and conduct transactions through other banks and FinTechs — thereby creating new opportunities for banks, FinTechs and aggregators to offer products and services from multiple providers on a single platform.

Banks are also set to benefit from Open Banking, with it leading to, the introduction of new channels, creation of a new wave of products and services, enhanced innovation and competition, and opportunity to increase revenue, amongst other benefits.

In this report, we explore how Open Banking will foster healthy competition within the banking ecosystem, with the opportunity for financial institutions and third parties to focus on strategies and development of innovative products and services that will win and retain customers in the digital age.

Competition in Nigeria’s banking ecosystem

The advent of digital technologies such as mobility, cloud computing, Internet of Things (IoT), intelligent applications, artificial intelligence etc. has led to a drastic change in customer behaviour, with customers having rising expectations for convenience, greater price transparency, personalized product and service offerings, real-time support, and swift response to service requests. This has led Nigerian banks, to rethink their business models and embark on digital transformation programs that have enabled them to develop the right capabilities to compete in the digital age.

In recent years, Nigerian banks have focused on customer experience and have built some digital capabilities (multi-channel experience, social media engagement, cloud computing, agile delivery etc.) in order to compete and remain relevant in the digital age. As a result of transforming digitally, banks have been able to attract new customers and grow, with Nigerian banks seeing an average growth of about 23% in customer deposits between 2017 and 2019. Banks have also been able to open up new channels (USSD, conversational banking and video banking) in order to compete with other banks and provide services to different customer segments.

In addition to competition between banks, the Nigerian FinTech industry has been evolving rapidly, with technology-focused startups and other new market entrants disrupting how the banking ecosystem operates. FinTechs and other digitally adept rivals are nibbling away at the big banks’ potential share of future growth, by providing innovative products and services through technology-driven applications which transform customer expectations and create opportunities across markets. FinTechs provide products and services such as payments (Paystack, Flutterwave, Interswitch etc.), savings and investments (PiggyVest, Cowrywise etc.), digital wallets (wallets.ng, Paga etc.), lending services (Migo, Carbon, Branch etc.), Super Apps (Opay), agency banking services (Paga, Opay).

Currently, banks have total control over all the customer information they collect, and they have leveraged this data to some extent to provide innovative and competitive products and services to customers. This is set to change in an Open Banking model, as customers will have control over their financial information and can choose to share it with other financial institutions or third party organisations in order to access products and services that are well-tailored to their needs.

While Nigerian banks have gained some level of digital maturity and have developed digital products and services to customers, they still face challenges in delivering superior experiences to customers due to the lack of standard APIs. This limits the collaboration with FinTechs and third-party organisations which then impedes innovation and the opportunity to solve real problems in Nigeria.

Open banking as a competition driver

Banks that have adopted open banking globally are delivering compelling customer experiences in order to gain and retain customers. They have taken advantage of open APIs to share and access rich data in a standard format that opens up a myriad of opportunities.

Banks are launching standalone apps that enable customers to view their accounts from other financial institutions on one platform. HSBC UK has launched a ‘Joined-Up banking’ offering with its ‘Connected Money’ app that allows its users to view their accounts, credit cards, mortgages and loans from up to 21 different banks and third party organisations in one place. The app also allows users to track their expenses and view insights based on their spending patterns, in order to make better financial decisions. HSBC signed up 300,000 new customers to its Connected Money app in the space of one year.

Data pipelines are being built in every direction as a result of customers’ requests and interactions with their financial services providers. This has created connected data structures where financial institutions and third parties can curate offerings that deliver a superior experience to customers. Customers, through the control they have over their data, have access to rich insight that they can use to understand their spending patterns and choose the products and services that are in line with their financial goals.

Banking marketplaces and aggregators that span financial and non-financial products and services are also beginning to emerge. These nimble marketplaces and aggregators appeal to digital customers through engaging and highly personalized product and service offerings. An example is Fidor which provides a marketplace for multiple financial needs. Fidor provides a direct-to-consumers digital store across digital channels, with products and services including P2P payments, social trading, personal finance, foreign exchange trading, savings and investments, global money transfer, insurance, cryptocurrency trading, crowdfinance and management tools from multiple banks, FinTechs, InsurTechs and TradeTechs using open APIs. Another example is Starling Bank in the UK which was built with Open Banking in mind right from the onset. This agile neobank has gone live with its marketplace, an ecosystem of aggregated financial products accessible through its app.

FinTechs and neobanks are not the only drivers of banking marketplaces. Traditional players such as Barclays bank have also launched their banking marketplace by aggregating personalized offers from multiple FinTechs, InsurTechs and TradeTechs, and providing it to customers on one platform. These nimble traditional players have invested in digital banking platforms with API management and analytics capabilities that will enable them to compete with other incumbents and challengers, through aggregation of the best products and services for customers.

Competition dynamics in an Open model

Effective competition creates benefits for customers in an open model. Financial institutions and third-party organisations also stand to benefit in an open model, depending on how they choose to play. Traditional banks must learn to compete differently if they are to remain relevant and retain customers in an ecosystem that features neo banks, FinTechs and other digital disruptors. They must evolve their customer experience capabilities and learn to be agile in their response to competition dynamics in an open model.

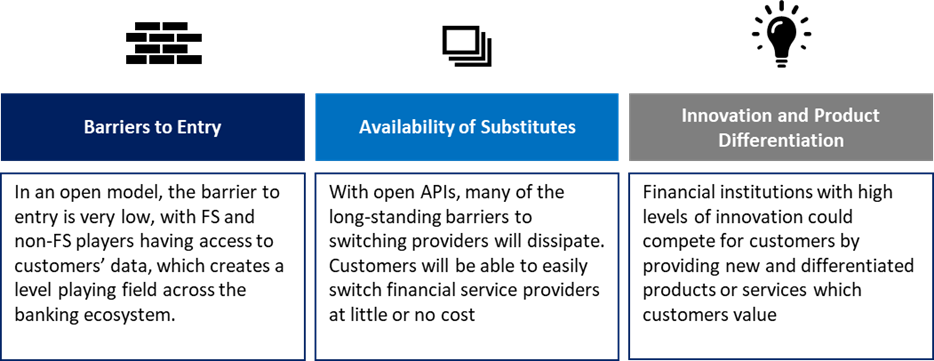

There are three key competition dynamics in an open model:

Barriers to Entry – The level of barriers to entry – and exit – is an important factor which can affect levels of competition over time. Years ago, traditional banks leveraged their established reputation, brand equity and networks to attract and retain customers, thus making it difficult for new entrants to join the market and compete effectively.

However, new technologies such as artificial intelligence, cloud computing, machine learning, robotic process automation and blockchain have been raising customer expectations and reducing entry barriers for FinTechs and non-financial institutions into the banking ecosystem. In an open model, the barrier to entry is even

lower, with FS and non-FS players having access

to customers’ data, which creates a level playing field across the banking ecosystem. Entry into the banking ecosystem can happen at three different levels in an open model:

- Entry of existing players into new sub-markets (e.g. a traditional bank leveraging customer data to provide Personal Financial Management – PFM or Robo-Advisory products and services)

- Entry of new players without existing banking presence into the market (e.g. a new Digital Telco expanding its service offerings and leveraging customer data to provide loans to products and services to Nigerian customers across channels)

- The entry of players with existing banking presence from other markets (e.g. a South African bank or FinTech player leveraging digital capabilities and customer data to provide financial customers)

To maintain stability and confidence in an open model, regulators across several markets have introduced and enforced standards and key requirements (such as licensing and operating requirements) to ensure that new entrants don’t breach the rules of participating in Open Banking.

The customer authentication feature

Availability of Substitutes – The existence and availability of substitute products are important to competition. With open APIs, many of the long-standing barriers to switching providers will dissipate. Customers will be able to easily switch financial service providers at little or no cost, thus making financial institutions focus on customer retention strategies and initiatives . The availability of substitutes will lead financial institutions and third-party organisations to be transparent with their pricing and deliberate in their product development efforts, in a bit to win customers over from competitors.

Innovation and Product Differentiation – Financial institutions with high levels of innovation could compete for customers by providing new products or services which customers value. Disintermediation of some banking products has been an important innovation to business models in recent years. This trend has allowed FinTechs and other smaller players to compete more effectively by accessing funding and wider distribution networks without the need to build scale (e.g. Wealthify, Carbon, Migo, Chipper Cash, TransferWise). Banks have also joined the trend by unpacking some of their products and making it available to customers across different channels (e.g Specta and i-invest by Sterling bank). In an open model, innovation and product differentiation will be very key, as the winning organisations would be the most innovative ones that are focused on providing compelling customer experiences.

How will open banking impact competition in Nigeria’s banking ecosystem?

The Nigerian banking ecosystem will be impacted by competition dynamics if it adopts Open Banking (Low barriers to entry, availability of substitutes, innovation and product differentiation). Nigerian FS players will have to respond to these competitive dynamics by rethinking their business model and placing customer experience at the centre of their product development and engagement efforts. Nigerian financial institutions will have to transform their value chain, embedding digital technologies and customer-centricity across strategy development, product development and management, omnichannel experience management, transaction management and customer service. This means data will be a very key resource, and the ability of banks and other organisations to compete will depend on how they mine this data to provide superior customer experiences.

Open banking presents a win-win partnership for all stakeholders within the Nigerian banking ecosystem (customers, traditional banks, neo banks, FinTechs and other non-FS players). FS and non-FS players can create new revenue streams, create a new wave of products and services, open up new channels and compete effectively. Nigerian Banks can serve as marketplace orchestrators, third party ecosystem participants, open banking platforms (banking-as-a-service) or referral platforms.

In addition to competing, Nigerian FS players will have to explore ways of reducing costs and increasing operational efficiency through outsourcing aspects of their front and middle office functions (e.g. credit scoring and processing, KYC, AML, customer experience management) to third parties in a connected ecosystem.

Nigerian FS players will also need to balance innovation with inclusion. With competitors springing up almost daily to challenge banks for their digital consumers, it is worth remembering that a large proportion of Nigerians are still unbanked and in need of simple and secure access to financial services. There are tremendous benefits to be gained by Nigerian financial institutions if they are innovative enough to cater to the unbanked population of the country. In developing digital and open banking strategies, FS players should continue to keep financial inclusion as a high priority area for innovation.

Next step for Nigerian financial institutions

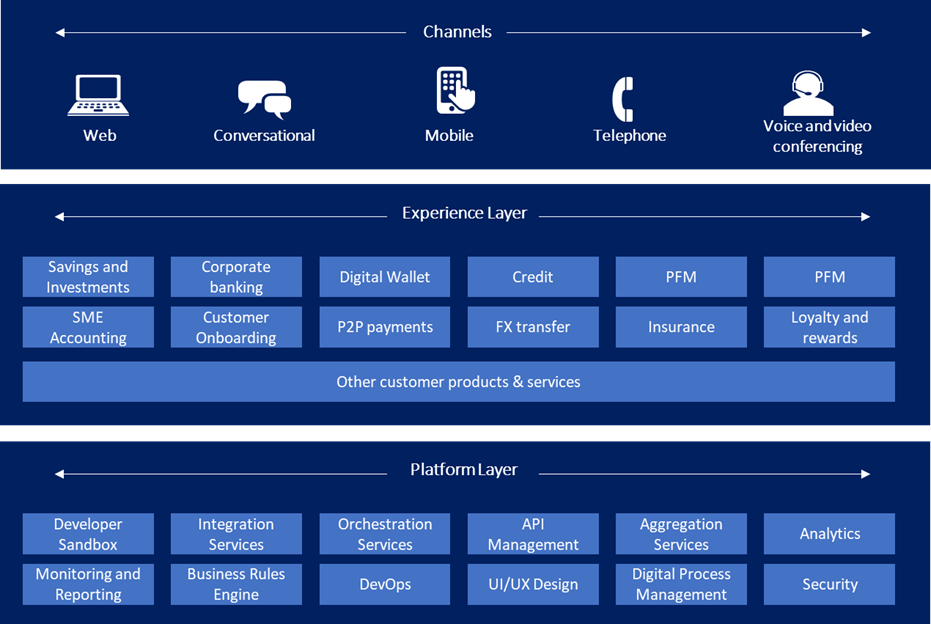

In order to be ready to take advantage of open banking, Nigerian banks will need to invest in digital platforms that have robust API management capabilities. The digital platforms should also possess containerization and microservices capabilities that will enable agile development of financial products and services and collaboration with different players within the banking ecosystem.

Conclusion

The adoption of open banking in the Nigerian banking ecosystem will drive competition, which is a good thing, as it encourages financial institutions to be innovative in their approach to creating value for customers. In order to take advantage of the benefits presented by open banking, financial institutions and other players will have to rethink their business model and develop digital capabilities that will enable them deliver compelling customer experiences.